Now that the Trump presidency has become a reality, his campaign pledge to slash taxes and impose tariffs on imports could usher in a period of inflation in the United States (the U.S.) and, subsequently, the global economy. These policies, if enacted, are expected to raise production costs, drive up consumer prices, and sustain a robust labour market in the U.S., ultimately leading to higher inflation. In this scenario, the Federal Reserve’s terminal funds rate—projected at 2.9% by 2026—could face upward repricing risks, delaying the full effect of rate cuts on global economies. We previously covered this, and you may read more at “How Would Singapore’s Property Market React to a Trump Presidency?”

In this article, we will discuss the divergence of mortgage rates in the current market by foreign and local banks, and the trajectory of mortgage rates in the near term. Read on to find out more!

Foreign Banks Take the Lead with Competitive Rates

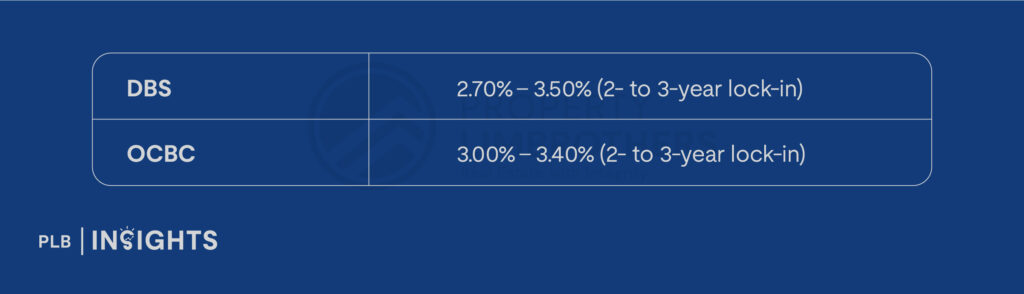

Even though uncertainties loom in the market, foreign banks operating in Singapore have decisively slashed their mortgage rates amid the shifting macroeconomic backdrop, offering highly competitive fixed-rate packages ranging from 2.45% to 2.55%. For instance, according to Redbrick Mortgage Advisory, the Bank of China currently offers a fixed rate of 2.45%-2.50% with a two- to three-year lock-in period, while Standard Chartered and CIMB follow closely with rates starting at 2.50% and 2.55%, respectively. This marks a significant divergence from local banks, whose fixed-rate packages remain higher, ranging from 2.70% to 3.40%.

Foreign banks in Singapore have made bold moves in the mortgage space:

While local banks held steady:

These competitive foreign bank rates have captured significant attention from borrowers, especially in a market where fixed deposit rates exceed mortgage pricing—a dynamic local banks deem unsustainable. DBS Chief Executive Piyush Gupta pointedly described such pricing as “not entirely sensible,” highlighting the disconnect between funding costs and mortgage pricing.

Local Banks Stand Firm: A Strategic Decision or Market Conservatism?

Singapore’s three major banks—DBS, UOB, and OCBC—have maintained a cautious stance, choosing not to follow foreign banks in aggressive rate reductions. Instead, they are closely monitoring market conditions before adjusting their mortgage offerings. At their respective Q3 2024 earnings calls, senior management from these banks reiterated their commitment to sustainability and prudent lending practices.

Piyush Gupta of DBS underscored the bank’s decision, stating: “Some of the mortgage pricing is not entirely sensible.” This perspective reflects a broader strategic calculus, as local banks weigh the risks of cutting rates against the potential for long-term margin pressures and funding mismatches. Similarly, OCBC CEO Helen Wong noted that rate cuts would depend on customer pipeline strength and broader relationship management rather than merely responding to competitive pressure.

UOB provided a more pragmatic view, acknowledging the need to remain competitive but emphasising a cautious approach to aggressive pricing strategies.

Implications for Borrowers and the Property Market

The divergence in mortgage rate strategies between foreign and local banks introduces a two-tiered lending landscape, with potential implications for Singapore’s property market. Lower rates from foreign banks could stimulate borrowing, increase demand for residential properties, especially among first-time buyers and upgraders. This increased activity might support price growth in the near term, further reinforcing the transition towards a seller’s market.

On the other hand, local banks’ conservative stance could act as a stabilising force, preventing excessive credit expansion that could lead to over-leveraging among borrowers. In a market already characterised by high property prices and stringent cooling measures, maintaining such a balance is crucial to avoid overheating.

Macro Context: Trump’s Policies and Their Ripple Effects

Trump’s presidency adds another layer of complexity to the global economic outlook. His pro-inflationary policies, such as tariffs and tax cuts, are expected to sustain robust employment levels and wage growth in the U.S. While this bodes well for the U.S.’ economic recovery, it also raises the spectre of persistent inflation, which could necessitate a higher terminal Fed funds rate.

In Singapore, where domestic interest rates are heavily influenced by global monetary policy and the U.S. dollar’s strength due to the nature of being an interest-rate-taker, these dynamics are likely to shape the trajectory of borrowing costs. The Monetary Authority of Singapore (MAS) has projected that the three-month compounded SORA will decline to around 2.5% by the end of 2025, down from its current level of 3.29%. However, this easing could be delayed if inflation reaccelerates, underscoring the importance of ongoing vigilance among market participants.

The Outlook: Opportunities and Risks in a Changing Landscape

As we move into 2025, the interplay between foreign and local banks’ mortgage strategies, coupled with macroeconomic shifts, will define the trajectory of Singapore’s real estate market. Borrowers may benefit from lower rates in the short term, but the sustainability of such pricing remains a critical question. For local banks, maintaining a disciplined approach may offer long-term resilience, even if it means sacrificing short-term market share.

Moreover, Trump’s economic policies and the evolving US inflation outlook will have far-reaching implications, potentially delaying the full benefits of global rate cuts. Singapore, with its robust regulatory framework and prudent banking sector, is well-positioned to navigate these challenges, but the road ahead will require careful monitoring of both domestic and international developments.

The trajectory of Singapore’s property market in 2025 will be influenced by several key factors:

1. Interest Rate Trends: Global interest rates, particularly those set by the U.S. Federal Reserve, significantly impact Singapore’s mortgage rates. Recent strong U.S. economic data have led to a reassessment of the pace and extent of Federal Reserve rate cuts, with some officials suggesting a possible pause in December.

2. Borrower Sentiment: Consumer confidence is crucial in driving property demand. In the U.S., despite recent inflation data, major stock indices have shown resilience, indicating sustained investor confidence.

3. Strategic Decisions of Market Players: The actions of financial institutions and developers, such as adjustments in mortgage rates and property offerings, play a pivotal role. For instance, foreign banks in Singapore have recently reduced mortgage rates, offering competitive fixed-rate packages between 2.45% and 2.55%, contrasting with higher rates from local banks.

Looking ahead to 2025, several developments warrant close attention:

- U.S. Economic Policies: President Donald Trump’s second-term economic agenda includes significant tax cuts, increased tariffs, and immigration controls, which could influence global economic conditions.

- Inflation and Employment Data: U.S. inflation has remained firm, with core CPI increasing by 0.3% in October, underscoring ongoing inflationary pressures.

- Additionally, the U.S. unemployment rate is projected to reach 4.5% by 2025, with payroll employment expected to rise modestly.

In this dynamic environment, adaptability and foresight will be essential for all stakeholders in Singapore’s property market. Monitoring these global economic indicators and policies will provide valuable insights for strategic decision-making.

In Summary

In summary, the trajectory of Singapore’s property market in 2025 will hinge on a complex interplay of global and domestic factors. The competitive mortgage strategies of foreign banks may spur borrowing and property demand, while local banks’ cautious approach could serve as a stabilising force. Meanwhile, the pro-inflationary policies of the Trump administration and their impact on global interest rates add another layer of uncertainty. As Singapore navigates these dynamics, the ability of market players to adapt and strategically respond to evolving conditions will be key to sustaining growth and stability in the property sector.

Let’s Get In Touch

Have questions about navigating the current property market? Don’t hesitate to reach out to us and our team of experienced consultants will be ready to assist with a personalised consultation.

Disclaimer: Information provided on this website is general in nature and does not constitute financial advice

PropertyLimBrothers will endeavour to update the website as needed. However, information may change without notice and we do not guarantee the accuracy of information on the website, including information provided by third parties, at any particular time. While every effort has been made that the information provided is accurate, individuals must not rely on this information to make a financial or investment decision. Before making any, we recommend you consult a financial planner or your bank to take into account your particular financial situation and individual needs. PropertyLimBrothers does not give any warranty as to the accuracy, reliability or completeness of information which is contained in this website. Except insofar as any liability under statute cannot be executed, PropertyLimBrothers, its employees do not accept any liability for any error or omission on this website or for any resulting loss or damage suffered by the recipient or any other person.